|

|

Post by seeshell on Mar 31, 2011 15:49:50 GMT 10

Hi FF

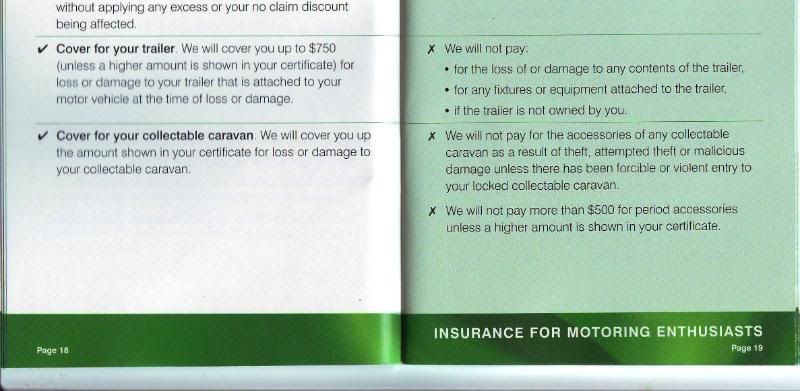

Yes I did get it what you were saying in your post "We will not pay more than $500 for period accessories unless a higher amount is shown in your ceretifcate" I was just wondering how it worked or if anyone had done that specifically - which it seems some have but with another firm.

I guess if I was fitting out my van with items from the late 60s it probably would be cheaper, but I'm not - going 40s - that makes it a bit dearer.

I haven't insured yet, since she's a driveway queen. But it won't be long before I have to - and I appreciate everyone sharing their experiences and details, most helpful.

Will be waiting with interest to see what response JBJ gets back.

Cheers

Seeshell

|

|

|

|

Post by JBJ on Mar 31, 2011 18:30:48 GMT 10

Hi All, Who would willingly deal with Insurance companies?  ? Bottom line is they have to make a Quid to satisfy the Muti Billion Company that owns them. But they all make their money by assesing an insurance risk, then putting a value on that, based on actuaric charts ( set by actuaries, who are pure mathematicians, sorta super smart people) All that bullshit aside, the problem we have been having is companies get too big, & need staff. You cant bring in new people that know your policies fully. So we get all sorts of answers. Before I post the reply I got from Rob at Shannons this arvo, I must stress that when you ring any insurance company, you should ask the person on the phone, their name, the branch office they are in, & then write that down. From Rob's phone discussion, they need to be able to track down the people giving out the wrong info. Every one of them costs Shannonns a policy. Sure go out & get competitive quotes, but at least be comparing apples with apples. I would also suggest that if you dont get the reply you wanted from Shannons, within the guidelines set in their email, that you contact Rob direct in their South Australia Office They want our business, make them perform.. When You ring, ask to be put through to him . The email response is as follows:: Good afternoon Mr watts Sorry for the late reply, just got all the clarification from the powers the be about insurance on historic caravans. Please see the outline below; As a reminder, please ensure all staff ask the appropriate questions regarding Caravan enquires/quotes. On a majority of calls we should be able to offer some Insurance solution – either Shannons (classic vans) or CIL. Points to remember, · All risk factors need to be taken into account and treated on a case/case basis · Classic vans are acceptable (subject to individually meeting our underwriting criteria) · Any van type used as a place of residence will be unacceptable · On a majority of enquiries from the forum we should be able to offer some Insurance solution, either being Shannons or CIL – details & circumstances depending. · This has been sent through to all branches around Australia, so all staff members should be aware of the underwriting guidelines. I hope this helps your forum and makes things a bit clear. Please contact me, if anything is amiss or unclear. Cheers, Rob Wheelwright | Senior Underwriter Shannons Limited 863-865 South Road Clarence Gardens SA 5039 ph 13 46 46 fax 1300 135 335 www.shannons.com.auWhat he hasn't said is that we are entitled to use our vans as we wish. If you read his point about about an van used as a residence will be unacceptable, then it follows that anything else would be acceptable. I hate these guys playing semantics, which is playing on words. A spade can never be a shovel, but why the hell cant they they say something in clear Aussie so we all can clearly understand. So bottom line, if you want a Quote from Shannons on your van, ring Rob directly on the phone number. He is a nice guy to deal with, trying to the best for his employers & clients. God I'm thirsty after this effort JBJ |

|

|

|

Post by firefighter on Mar 31, 2011 19:20:03 GMT 10

Part of jbj statement What he hasn't said is that we are entitled to use our vans as we wish. If you read his point about about a van used as a residence will be unacceptable, then it follows that anything else would be acceptable. Looks like your cannot use your van if you are with shannons to sleep in it at vintage caravan events or go on holidays ? f/f ;D ;D ;D ;D

|

|

|

|

Post by JBJ on Mar 31, 2011 19:26:26 GMT 10

Hi Firefighter,

Thats not as It was meant.

Rob has been strongly commenting that we can use as we wish, as long as we are NOT PERMANENTLY living in the van.

I guess it depends again on interpretation.

I'll send another email requesting a definition of "permanently living in a van"

It goes on & on.

JBJ

|

|

|

|

Post by JBJ on Mar 31, 2011 19:35:40 GMT 10

Hi All,

My reply to Rob at Shannons.

I'm as sick of the crap going down as anyone, but if I don't push the point with them we really dont know where anyone stands if an accident/insurance claim occurs.

I cancelled my insurance with Shannons a few years back because of the same answers, & then went back to them when I was told what I wanted to hear.

Pretty scary to a peasant.

MY REPLY

Hi Rob,,

Lots of nothing definite in your reply unfortunately.

I know you guys have to play it your way.

However, what defines "permantly living" in a van. Several nights, a long trip of several months, or a permanent postal adress in a caravan park???

Why is CIL in the equation?? We were talking of dealing with Shannons. CIL equates GIO equates anyone.

What is the underwriting criteria relating to acceptance of our vans??

I'm looking for something definite in your reply, not semantics or vague answers.

Sorry Rob, back to you

Dennis

|

|

|

|

Post by seeshell on Mar 31, 2011 20:09:33 GMT 10

Hi All

I have to say the whole thing around the insurance baffles me - in most cases the nominated value of a vintage van is less than a modern van so it seems unlikely that it is about them being stratospherically costly by comparison to insure.

And if insurance is based on risk then you would have to say that people who *love* their vans like people here do are likely to be extremely careful - and probably reasonably low risk.

Regardless, in most cases people want a nominated value. And you would think that would be good for insurance companies who don't have too many examples of rare vans to gauge value on.

Given many people are going for a moderate nominated value, insurance companies are not out of pocket by insuring us. We pay for what we want. Also, if the nominated value is low, there's little risk of high repair costs; they'll just write it off (god knows it doesn't take much to rack up a repair bill).

Why do they distinguish between old and newer vans at all - if it's good enough to be roadworthy and registerable then surely that's the end of it? If anyone does know, I hope they share.

Probably asking dumb newbie questions -

Seeshell

|

|

|

|

Post by seeshell on Mar 31, 2011 21:47:49 GMT 10

Hi Rod

Re: GIO definitive answer - some people appear to feel they have. I'm already with them for our other insurance so that's going to be my first stop. When I do that, I'll see if I can get something to share here.

As to the Lowlife that might knock stuff off - I'm perfectly ok if I'm only covered while the van is locked. More fool anyone that is leaving groovy stuff out of doors unsupervised - sadly.

Cheers

Seeshell

|

|

|

|

Post by lovshack on Apr 2, 2011 11:09:09 GMT 10

g'day all, finally sorted the insurance thing out. ;D rang shannons and was told they don't do vintage vans [ the sooner they get their chet together the better  ] and passed us onto CIL... their sister, brother,mother company, whatever, that deals with caravans. they couldn't have been more helpful and the people we spoke to actually knew what we were talking about vintage van wise... and.. they were very conversant with all facets of the hobby etc...amazing.  anyway, after the usual request for photos etc, we are in business again ;D one thing to look out for in 'anyones' policy....check what they say about modifications ie wheels, suspension, draw bar ,wiring, interior mods etc... ANYTHING NOT DONE BY THE MANUFACTURER.."could" void the policy and you are in deep, deep doodoo if the chet hits the fan. cheers dave |

|

|

|

Post by seeshell on Apr 2, 2011 16:26:29 GMT 10

Hi Dave

Yes that was the statement that worried me too - "originally installed by the manufacturer" - since many of us do renovations, or over time have to replace equipment in these vans, unless you're lucky enough to get a "shed find".

Cheers

Seeshell

|

|

dave01

Full Member

MR ROADHAVEN

MR ROADHAVEN

Posts: 234

|

Post by dave01 on Apr 2, 2011 19:52:00 GMT 10

After reading all these yes we do no we dont comments about shannons insuring v vans i received i definitive YES we do from shannons last week. I pointed out these comments to which the reply was....read the fineprint, some policys cover the van for shows and v van runs only, while others including mine cover the van for any type of use. Interestingly my initial inquiry was met with no we dont, but on asking me if i knew a certain forum member i was told yes we do. I,m at present with the racv but want to increase the value of my policy, so queued up to do so only to be told it can only be done over the phone...wot the? Might be easier to leave it in the shed. Cheers, Bewillderd dave.

|

|

|

|

Post by shaneandsimoen on Apr 7, 2011 22:14:11 GMT 10

I have just insured my van today with no trouble with Shannons.

Having 5 cars and house with them they were happy to insure.

The chap ( David From Sydney) told me the limited use applied for couple days a month or ok to use say for a week or two each year.

Shane

|

|

|

|

Post by Daggsey on Apr 8, 2011 0:57:51 GMT 10

|

|

|

|

Post by cobber on Apr 8, 2011 6:19:32 GMT 10

Don't like your chances Daggsey  ;D ;D ;D  Cobber. |

|

|

|

Post by Daggsey on Apr 8, 2011 13:41:16 GMT 10

|

|

|

|

Post by JBJ on Apr 8, 2011 13:50:36 GMT 10

|

|

|

|

Post by cobber on Apr 8, 2011 15:07:18 GMT 10

G'day Dave, Oh dear........ I just rang GIO to see if they would insure Ol' 36 Or Driftwood.............. they won't..... because neither is a branded make of caravan. AND...... CIL won't insure either of them because they are occasionally put on "show". AND.... MHIA want me to take both 'vans to a registered caravan dealer to have them valued. AND.... NRMA Veteran, Vintage & Classic vehicle Insurance won't touch either because their chassis is partly timber. Have had insurance on Ol'36 with Shannons since 2007. No insurance on Driftwood or the Newcastle van for the last few years (except the CTP that comes with the tow car.... that should open up a new can of worms  ) Cobber. |

|

|

|

Post by JBJ on Apr 8, 2011 16:09:05 GMT 10

Hi All,

And meanwhile the worm keeps turning. A phrase I remember from something in an English class.

I know I keep repeating myself, but this is exactly where our problem lies.

Inconsistency, & until it is properly defined it doesn't matter which company you go to, you take pot luck if you need to make a claim.

I guess no one will never agree on the worth of pursuing this thread either, but I'm going to keep plugging away at Shannons.

I'll ring Rob next week.

JBJ

|

|

|

|

Post by cobber on Apr 8, 2011 17:56:33 GMT 10

If anybody gets sick of reading this thread, four pages long........... you can always go to this thread. Page 5 is interesting Cobber. |

|

|

|

Post by sharpie on Apr 30, 2011 20:37:23 GMT 10

Hi JBJ Keep plugging away because we do need something positive so we all know where we stand. Thanks for your efforts.

Cheers Sharpie.

|

|

|

|

Post by JBJ on May 1, 2011 0:11:05 GMT 10

Hi,

I've had no further reply from Shannons since I questioned the answer I was given, & mentioned that I thought it was a nothing reply.

So still havent achieved anything

JBJ

|

|

|

|

Post by vernon on May 1, 2011 18:48:24 GMT 10

Hi all, and thanks to JBJ for posting this thread,

After this thread as a lot of members, we too rang Shannons and questioned our

Insurance position. They were great and actually suggested other avenues for us, because the way we are choosing to use our van didn't fit into their existing criteria, our annex would not now have been covered (which when we took our insurance out nearly two years ago they said it would be covered) etc.

They would however insure us for moving of a van, where other companies were not interested, because we have had a long relationship and multiple policies with them. Whilst we do not have Vernon now with them we have kept other insurance polices as they offer us other perks that we have found other companies don't.

Shannons have been very clear and transparent with us as to what they do not cover . (This worked for our situation).

JBJ as Joda says "Ummmmmmmmmmmmm cloudy is the future".

Cheers Des and Kel

|

|

jann

New Member

Posts: 39

|

Post by jann on May 4, 2011 18:25:08 GMT 10

I also rang Shannons and they wouldnt insure my van cause they felt i wasnt a car enthusiast. So i rang MHia and they were willing to insure my van + annex, but would need photo's inside & out. Thats fine with me i have nothing to hide but I'll also be calling other insurance companies about the cost.  I paid a cheap price for my van, way under value! when looking on ebay etc so i double my price on insurance. I still have renovations to do like the axel and few curtains to put up but what value do you place on such a van?? How much is my van really worth? the price i brought it for or what the prices are going on the market today? |

|

|

|

Post by seeshell on May 5, 2011 6:45:03 GMT 10

Hi Jann

For me, I think it's probably closer to what it would take to replace it than what I paid for it - we've done a heap of work and have more to do.

Cheers

Seeshell

|

|

|

|

Post by Don Ricardo on May 5, 2011 10:48:14 GMT 10

Hi Jann,

I think the principle with insurance is that you insure the van for whatever it would cost to replace your van as it now is with improvements and all mod cons, not what you paid for it (especially if you got it cheaply). So if you had to buy a similar van in good restored condition in a hotly contested Ebay auction, what would it cost you?

The other thing to watch is that you need to make sure that your annexe (if you have one) and contents are listed and sufficiently covered. The standard insurance policy for our van covers $500 worth of contents, but when you include all the gear you take with you when you travel (clothes, bedding, kitchen bits and pieces, assorted camping gear, electronic gear, etc) it doesn't take long to get over $500.

If you want another insurer to try, talk to GIO. We insured our 60 year old van with them about 4 years ago - minimal trouble in arranging the policy and reasonable cost. We haven't had a claim yet, so can't vouch for that side of things, but then our aim is never to have a claim! ;D ;D ;D

Don Ricardo

|

|

jann

New Member

Posts: 39

|

Post by jann on May 5, 2011 13:52:07 GMT 10

Thanks so much for your advice seeshell and Don.

I gave GIO a call today and i was very happy with the premium for the year, half the price of what Mhia quoted me.

I also managed to insure my annexe & contents ( $2000) extra on top.

They also said to me when i finish changing the axel over and redecorating give them a call to up the value of the van.

Thanks again i feel so much better now that my caravan is insured for whats its worth!! ;D

|

|

?

?

] and passed us onto CIL... their sister, brother,mother company, whatever, that deals with caravans.

] and passed us onto CIL... their sister, brother,mother company, whatever, that deals with caravans.